Futures Market: Overnight, LME copper opened at $9,686.5/mt, rose initially and peaked at $9,713/mt, then fluctuated downward during the session and bottomed out at $9,647.5/mt. It rebounded slightly towards the end of the session and closed at $9,670/mt, down 0.26%. Trading volume reached 13,000 lots, and open interest reached 293,000 lots. Overnight, the most-traded SHFE copper 2507 contract opened at 78,600 yuan/mt, peaked at 78,690 yuan/mt shortly after the opening, then fluctuated downward and bottomed out at 78,360 yuan/mt during the session. It rebounded steadily towards the end of the session and closed at 78,560 yuan/mt, up 0.04%. Trading volume reached 20,000 lots, and open interest reached 182,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) Ivanhoe Mines announced that after a temporary production suspension lasting one month, its Kakula West copper mine in the Democratic Republic of the Congo (DRC) has resumed production. This underground mine is part of the company's Kamoa-Kakula copper joint venture. On May 18, the mine was forced to suspend production due to severe water inflow caused by seismic activity in the region. Ivanhoe has set a new production target for the Kamoa-Kakula joint venture in 2025: 370,000-420,000 mt of copper concentrate. Based on the midpoint, this projection represents a 28% decrease from the previous production target of 520,000-580,000 mt set in January.

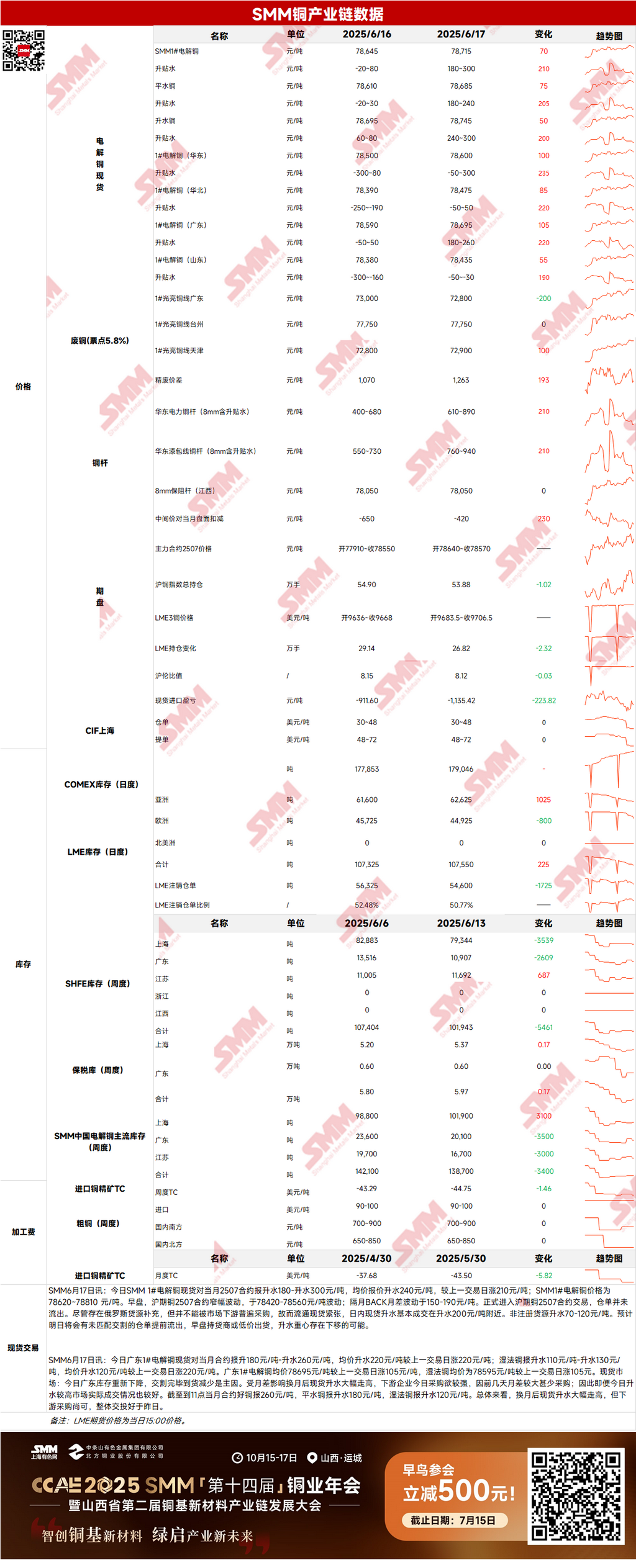

Spot: (1) Shanghai: On June 17, SMM #1 copper cathode spot premiums against the front-month 2507 contract were reported at 180-300 yuan/mt, with an average premium of 240 yuan/mt, up 210 yuan/mt from the previous trading day. The SMM #1 copper cathode price was 78,620-78,810 yuan/mt. In the morning session, the SHFE copper 2507 contract fluctuated rangebound between 78,420-78,560 yuan/mt. The price spread between futures contracts (BACK) for the next month fluctuated between 150-190 yuan/mt. Trading officially commenced for the SHFE copper 2507 contract, but warrants were not released. Despite the supplement of Russian supply, it was not widely purchased by downstream market participants, leading to tight spot supply. Spot premiums were mainly transacted around 200 yuan/mt during the day. Non-registered supply premiums were 70-120 yuan/mt. It is expected that unmatched delivery warrants will be released early tomorrow, and suppliers may sell at lower prices in the morning session, with the possibility of the premium center moving downward.

(2) Guangdong: On June 17, Guangdong #1 copper cathode spot premiums against the front-month contract were reported at 180-260 yuan/mt, with an average premium of 220 yuan/mt, up 220 yuan/mt from the previous trading day. SX-EW copper premiums were 110-130 yuan/mt, with an average premium of 120 yuan/mt, up 220 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 78,695 yuan/mt, up 105 yuan/mt from the previous trading day, and the average price of SX-EW copper was 78,595 yuan/mt, up 105 yuan/mt from the previous trading day. Overall, spot premiums rose significantly after the contract rollover, but downstream purchasing was moderate, and overall trading activity was better than yesterday.

(3) Imported copper: On June 17, warrant prices ranged from $30 to $48/mt, with QP in June, and the average price remained unchanged from the previous trading day. B/L prices ranged from $48 to $72/mt, with QP in July, and the average price remained unchanged from the previous trading day. EQ copper (CIF B/L) prices ranged from $4 to $18/mt, with QP in July, and the average price remained unchanged from the previous trading day. Quotations referenced cargoes arriving in late June and early July. The US dollar copper market remained sluggish. Affected by the shortage of copper concentrates, JX Nippon Mining & Metals Corporation issued an official announcement declaring an upcoming production cut plan, with the specific reduction volume yet to be determined. The LME copper backwardation structure continued to widen in the far months, and a normalized backwardation structure may become a trend in H2. Overall, suppliers mostly chose to hold back cargoes, while downstream consumption willingness was also weak, resulting in weak supply and demand in the market as a whole.

(4) Secondary copper: On June 17, the price of secondary copper raw materials decreased by 200 yuan/mt MoM. The price of bare bright copper in Guangdong ranged from 72,700 to 72,900 yuan/mt, down 200 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,263 yuan/mt, up 193 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,170 yuan/mt. According to the SMM survey, the actual implementation of "reverse invoicing" varied across different cities and districts in Anhui Province, leaving local enterprises temporarily unclear on how to respond and handle the situation. As a result, some enterprises reported that open-hearth furnaces had been halted for a long time and would resume production only after the unified implementation of policies in Anhui Province.

(5) Inventory: On June 17, LME copper cathode inventories increased by 225 mt to 107,550 mt. On June 17, SHFE warrant inventories increased by 7,490 mt to 54,541 mt.

Price: On the macro side, data showed that US retail sales declined more than expected in May, but consumer spending remained supported by robust wage growth, and the US dollar index weakened. However, as the market digested the data, the US dollar reversed its losses, and copper prices first rose and then fell. On the fundamental side, on the first trading day of the SHFE copper 2507 contract, no warrants were released. Although Russian cargoes were supplemented, they were difficult to be widely purchased by the downstream, leading to tight spot cargo circulation. It is expected that unmatched delivery warrants may be released in advance tomorrow, and suppliers may sell at lower prices in the morning session, with the risk of a downward shift in the premium center. In summary, given the presence of bearish factors, it is expected that there will be limited upside potential for copper prices today.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]